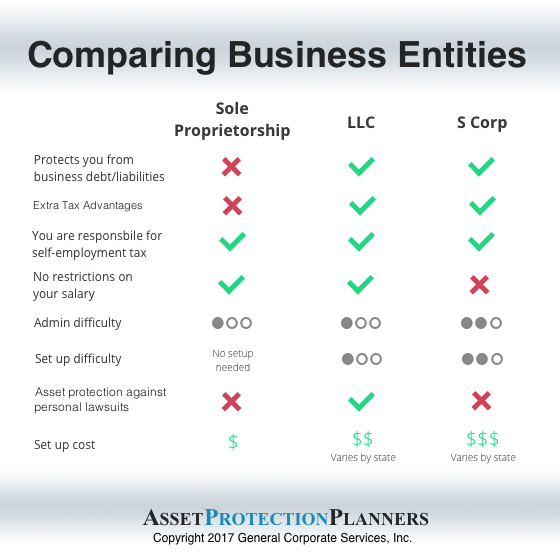

Sole proprietorships and partnerships offer no protection of personal assets from business liability exposure. With these business types, a lawsuit against your business may expose your home, car, bank account and everything you have worked so hard for. Therefore, entrepreneurs owners should always formalize their businesses by incorporating or forming LLCs. Legal vehicles shield the personal assets of the shareholders or members from debts and liability of the business. Corporations and LLCs form a separate “person” from the owner. That separation is called the “corporate veil.” The veil gives owners and principles a shield against the legal liabilities of the business.

Forming a business entity is a good start. It is essential that you form form your company properly. Improperly formed business entities do not hold up in court. In addition, individuals must establish, fund and operate the business properly in order to maximize asset protection benefits.

Types of Business Entities

The most common form of business entities are corporations and LLCs. Business owners use these entities for multiple advantages. There are tax benefits. As stated previously, they offer protection from lawsuits against the business. Statutes usually don’t allow attorneys, medical practitioners, CPAs, etc. to form standard entities. Instead, they need to form professional corporations, professional LLCs or create a limited liability partnerships. Typically, the law requires that licensed members of a particular profession are the owners of these entities.

Corporations

Corporations can offer outstanding protection for shareholders, officers and directors. Thus, these entities work well for businesses with multiple owners and employees. There are extra tax deductions, such as those for healthcare plans and medical expenses. Accountants typically recommend against using corporations to own real property. There are detrimental tax consequences compared to LLCs. Plus, creditor law considers the shares as personal assets. Creditors can seize them and sell the stock to satisfy judgments. So, shareholders need to protect their stock by holding them in trusts or LLCs as part of a personal asset protection strategy.

Limited Liability Companies (LLCs)

A Limited Liability Company also offers personal liability protection from business transactions. It shields the managers and members (i.e. owners) from liability. The LLC also has fewer business formalities than does the corporation. By default, LLCs are pass-through tax entities. Many experts highly recommend LLCs for owning real estate. This is due to the fact that provisions prevent creditors from seizing LLC interest to satisfy a judgment. Should someone sue a company member the company and the assets inside are secure. Thus, property and other business assets held in an LLC is protected from personal liability of the managers and members.

Maintaining Business Entities

We have established Corporations since 1906 and LLCs since the laws became widespread in 1994. So, we can form these entities quickly and easily. We establish them for clients at a nominal cost for the protection they offer. In order to maximize the benefits of a business entity, the owners will perform simple formalities. Principle parties hold annual shareholder and director meetings for corporations. LLC owners sign an LLC operating agreement. Meeting the simple requirements help maintain separation of personal and business affairs. The government requires that someone files annual information statements for the business entities. The annual filings are submitted to the state in which they are formed and in which they operate.

Keep business and personal funds separate. You would not pay your personal light bill with your corporate checkbook. More specifically, if the funds of a business are used to pay personal debts or bills, or vice versa, the courts will call the company your “alter ego.” This legal theory could be used to challenge the entity and pierce the corporate veil. Thus, the separation of corporation and personal funds keeps the corporate veil stronger. This, in turn, gives you stronger legal protection. Additionally, professional accounting and a proper business presence should be part of operating and maintaining your business entity.

Conclusion

Small business owners should be especially concerned with protecting personal assets from liability of the business. Without the proper legal structure, contract dispute, torts, employee lawsuits, company vehicles, sexual harassment and many more business related liability hazards can pose threats to one’s personal assets.

So, form a corporation or LLC to own your business. If you own more than one business, you do not want a lawsuit against one business to take the assets of the other business. So, to separate one business from another, set up one company per business.

If you run a business with substantial assets, do the following. Operate your business in one company. Then, own the assets that the business uses in a separate LLC. Your operating business will lease the equipment from your LLC. Therefore, when someone sues your operating business there will be few to no assets to take.

For more information you can complete the consultation form on this page. Alternatively, you can use the numbers above to speak directly with a consultant to discuss your needs.