A spendthrift trust grants an independent trustee the power to determine how the trust funds are spent for the benefit of the beneficiary. The trustee has a duty to act in the best interest of the trust beneficiary. The spendthrift trust was originally one that people set up for a person who has a history of reckless spending. The trustee has oversight over the use of trust resources. With such an arrangement, the beneficiary does not squander his or her inheritance. More commonly today, professionals insert spendthrift provisions into trusts to protect assets from creditors. That is, the trustee can distribute funds to or for the beneficiary or beneficiaries but not their respective creditors.

People also use the spendthrift trust as a tool for financial planning. Its slang name – “spendthrift” – should not lead anyone to underestimate it. The spendthrift trust legal strategy can provide for the transfer of wealth. Plus, it can give the benefit of preservation of assets during one’s lifetime. There are a number of versions of it. As indicated above, one can apply them to financial planning challenges beyond saving the family fortune from the reckless heir.

Two Reasons for the Growing Popularity of Spendthrift Trusts

There has been growing interest in the spendthrift trust for two reasons.

One is the unprecedented amount of wealth which estates will pass along to the next generations during the next 25 years. Yet, as the RBC Wealth Transfer Study found, relatively few among the benefactors feel they are prepared.

For a specific group of those benefactors, the spendthrift trust can provide a proven passageway through the complexities and pitfalls of that process. It also is a way of bypassing the public ordeal of probate. The terms and conditions are private. That can be important to families.

The second reason for the growing interest in spendthrift trust is the litigiousness of American society. The boundaries between business and personal have become blurred. Creditors, for example, rush to court to seize the personal assets of the owners of distressed businesses. And, in civil lawsuits against professionals such as medical doctors or lawyers, defendants push for the right to attach their homes, cars, and stock portfolios. One version of the spendthrift trust – the Domestic Asset Protection Trust (DAPT) or the self-settled spendthrift trust – can prevent that. In addition, the DAPT can be useful in reducing taxes and in providing income for retirement.

$68 Trillion Will Pass Among Generations

During the next quarter of a century, according to the Cerulli report, there will be a transfer of $68 trillion throughout 45 million households.

That is the common thread. But there are many different kinds of benefactors. Actually, no two are exactly alike.

There is a group among them facing the soul-wrenching concerns which the spendthrift trust addresses.

Those concerns come in three forms.

Irresponsible beneficiaries. Their children or someone else they care about cannot “handle money.” There is anxiety that the wealth they inherit will attract con artists who will dupe them. Or they can blow their way through the fortune. They might marry the kind of spouse who can help them do just that.

Special-needs dependents. They have disabilities such as autism or bipolar disorder. An inheritance could make them illegible for Medicaid and Social Security Supplemental Income (SSI).

Professionals targeted for lawsuits. There are also those future beneficiaries in lines of work vulnerable to lawsuits. That litigation can reduce the family inheritance to zero.

What is a “Trust?”

Essentially, a “trust” provides the legal framework which assigns “property” to one party to manage for the benefit of another. That term “property” can refer to actual property such as 340 acres of land in Wyoming. But in law, it also can include investments such as stocks and bonds, patents, trademarks, and so on.

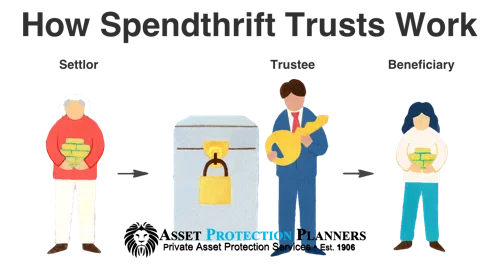

What the trust sets up is a three-way relationship:

- The Trustor or settlor. Simply put, that is the benefactor; the one who sets up the trust. In practice, it is typically the person who hires the professional person or organization to establish the trust.

- The Trustee. That is the institution or person whom the benefactor designates or state law determines receives the property to oversee.

- The Beneficiary. That is, the one who benefits from the property in the trust.

Primarily it is state statutory law which pertains to establishing and administering trusts. The laws vary from state to state, sometimes significantly.

Choosing the Right Place to Set Up the Trust

Therefore, benefactors might “shop around” for the state or country that offers terms and conditions which are the best fit for their particular situations. Nevada is at the top of the list for spendthrift trusts. Its favorable treatment ranges from not being subject to state income tax in Nevada to none of the usual processing fees.

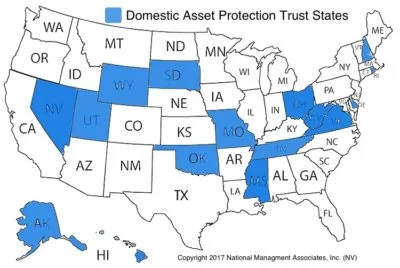

In regard to the DAPT, only 17 states allow it or what some refer to as “the selfie trust.” Those states allowing DAPT range from Alaska to Nevada. As with all state law, what applies in one state might be quite different from what is law in another state.

The strongest trusts worldwide that provide asset protection are those in the Cook Islands (south of Hawaii) and Nevis (in the Caribbean). The trustees in these jurisdictions are not subject to the order of foreign courts. So if, for example a US court says “give me the money,” the foreign trustee (a.k.a. our Cook Islands law firm) can say, “you don’t have jurisdiction down here,” and the money safe and secure.

How a Spendthrift Trust Works

There are many kinds of trusts that people use in estate planning. They are not mutually exclusive. A benefactor can set up any number of them simultaneously.

One kind could be for the offspring who has proved to be financially responsible. That particular trust could provide a lump sum payment of the entire inheritance. Alternatively for, for example, the trust could distribute increments of 10% of the trust corpus annually over the next 10 years. No, not all heirs should be treated the same.

For the less responsible offspring, there is the spendthrift trust. Initially, people created spendthrift trusts to manage the transfer of wealth in a way that gave the settlor peace of mind. It ensures that the beneficiary will not be able to “squander” the total inheritance, be the target of predators, or leave asset vulnerable to plunder by third parties such as creditors.

Beneficiaries

The settlor puts property in trust. When the settlor dies (or before) the beneficiary becomes another person. That person may or may not be a child or a blood relative. The beneficiary could be a loyal housekeeper who has little experience managing money.

Then the benefactor assigns a trustee to manage the trust. Depending on the wishes of the benefactor and/or state law the trustee could be an institution such as a bank or a person such as a lawyer, relative, or friend. The trust pays the trustee for such services. Some view that expense as a drawback of this financial instrument, but usually the fees are extremely reasonable. Don’t like the trustee? Great. Fire them an hire another.

Lifetime Spendthrift Trust

The settlor custom-makes the terms and conditions for how the funds will distributed. One popular version is the lifetime spendthrift trust. This type of trust provides for the beneficiary for a lifetime. The terms can vary.

Typically, there might be a monthly distribution to the beneficiary of, for example, $3,500 for the lifetime of the beneficiary. How the beneficiary spends it may be totally discretionary. Or, there could be the stipulation that it is can only be applied to building a real estate practice in the state of Maine. Another possibility is that none of the $3,500 monthly distribution is given directly to the beneficiary. Instead the trustee uses it to cover the bills of his or her daily living. That is routine when the beneficiary suffers from addiction.

No matter how the distribution is made, only those funds, not the assets in the fund per se, can creditors attach through collections or the courts. Essentially, the principal remains untouched. Yes, creditors legally can go after that $3,500 monthly distribution. That is important for those doing estate planning to understand this.

Flexibility

The spendthrift structure has flexibility. The benefactor might make a provision that in extraordinary circumstances such as a medical emergency there could be a larger distribution or even a dipping into the principal. That will pay the bills.

In addition, there could be the stipulation to only keep the trust in effect until the beneficiary is, for example, 50 years old or has been married five years.

Over time, other applications have emerged for the spendthrift trust. There are three common ones.

The offspring might be in profession in which lawsuits are standard. The trust’s structure ensures that the inheritance will not be seized to pay verdicts and settlements.

Or, one can use the trust to facilitate a special needs’ child’s eligibility for needs-based benefits. This can range from Medicaid to Supplemental Security Income (SSI). That is done through a version of the spendthrift trust known as the “wholly discretionary trust.” The trustee has 100 percent decision-making authority about how much, if any, of the funds that the trust will distribute. Without Medicaid the cost of the special-needs dependent’s treatment and maintenance can decimate the family wealth.

The trust can also prevent the courts from treating an inheritance as marital property. The trust makes it off-limits in a divorce. In a sense one could consider it a type of prenuptial contract but put together on a unilateral basis. Traditionally, prenuptials involve two parties.

Spendthrift Clause

So useful the spendthrift legal framework has been that many estate planners routinely insert a spendthrift provision or clause in other kinds of trusts they set up. What is important is the language or how the professional person words the clauses. Without the appropriate language the courts could invalidate the trust.

Here is an example of that kind of provision, provided by Mary Randolph, JD in an article published in AllLaw.com:

“Except as otherwise provided in this Trust Agreement, all payments of principal and income which as payable, or will become payable, to the beneficiary of any Trust created by this Agreement shall not be subject to anticipation, assignment, pledge, sale, or transfer in any manner.

“Nor shall any beneficiary have the power to anticipate or encumber any such interest.

“Nor shall any such interest, while in the possession of the Trustees, be liable for, or subject to, the debts, contracts, obligations, liabilities or torts of any beneficiary.

“Such interests shall also be free from any claim, control, or interference of the spouse of a married beneficiary, or the parent of a beneficiary.”

Three Ways the Courts Can “Invade” a Spendthrift Trust

There is that ancient adage: Mankind plans, the gods laugh.

That wisdom also applies to even the legally valid spendthrift trusts. Despite the best efforts of the benefactor and the experience of the lawyer, there could be what is known as the “invasion” of assets. Yes, that reckless offspring could wind up exposing the wealth to access by third parties. We have address many about pros and cons. Let’s talk about some cons and some downsides of the domestic spendthrift trusts.

Here are some of the ways the assets can be siphoned off:

- Failure to pay child support or alimony. The courts could order those payments withdrawn from the assets. Retroactive and future payments could “wipe out” the assets.

- Debts due to state and federal governments. That could take the form of taxes not paid or a fine that is imposed as part of a sentence in a civil legal action.

- Payment due those who have provided services to the beneficiary associated with the trust.

How to Set Up an Spendthrift Trust

The transfer of wealth is not simply a legal transaction and a financial matter. Benefactors, of course, need a seasoned lawyer specializing in estate planning. In addition, there are the tax implications. If the attorney does not have that additional expertise in taxes, then the benefactor must also consult with an expert in tax law. Since tax laws continually change the benefactor and tax expert must factor in future possibilities in creating the terms and conditions.

But, beyond the legalities and financials associated with transferring wealth there are the psychological matters. Those apply to the entire family context. That context is frequently a continuum extending from blood relatives to others considered “family” because of service or an emotional tie. All that might be labeled the “psychology of money.”

Professional Advice

That is why some financial planners recommend family discussions prior to creating any trust. In fact, the BBC Wealth Transfer Study found a correlation between preservation of the wealth and preparing the beneficiaries about what is planned. Yet, Cerulli documented that in less than half of the trusts set up do financial planners get to know the benefactor’s children and grandchildren.

The tendency might be to assume: The money is mine, therefore all the decisions what to do with it are mine.

However, there might be less tension in the administration of the spendthrift trust if the benefactor probed what those who would be inheriting wealth felt about that and how they envisioned using it.

After those kinds of discussions, for example, the benefactor might decide that a spendthrift trust would not be appropriate for the oldest child. She was already engaged in tutoring female entrepreneurs in developing economies. The benefactor might decide to leave her funds in the form of a lump sum to support that mission.

What is a DAPT?

DAPT (Domestic Asset Protection Trust) is a relatively new legal tool to protect wealth while a person is alive and probably working. In addition, it can provide a source of income during retirement. The person setting up the DAPT and the beneficiary are the same. By the DAPT’s structure, there are also other beneficiaries.

High net individuals and those whose line of work makes them vulnerable to civil litigation find this option useful. It puts assets in the trust off-limits in civil judgments, from the long reach of creditors, and in a divorce. In addition, the new tax law makes it attractive, at least until 2026.

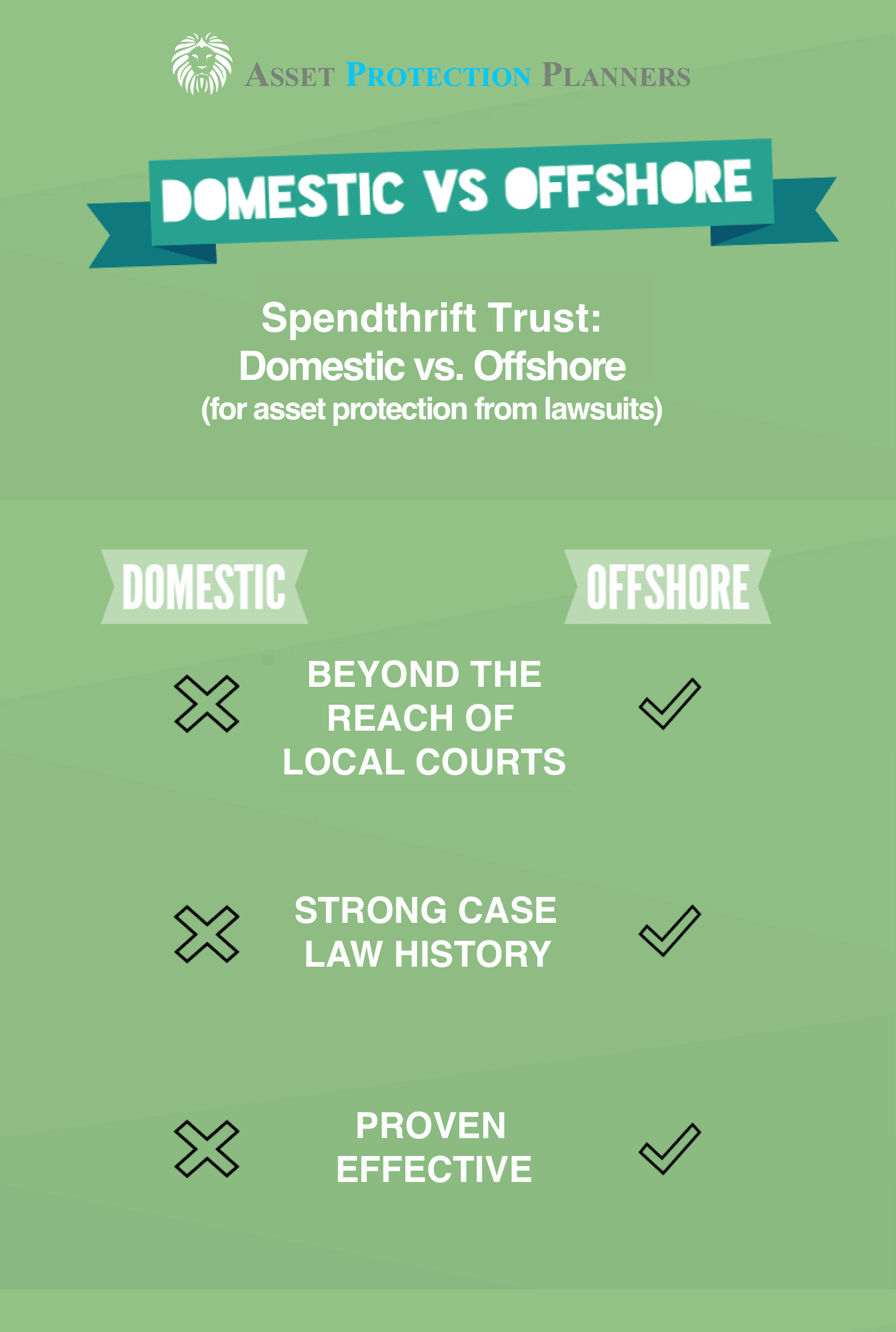

Offshore Spendthrift Trust

An alternative to this U.S. based approach is the Foreign Asset Protection Trust or, what is commonly referred to as an “offshore trust.”

Here is why the offshore trust protects assets more effectively than its domestic counterpart:

- The offshore trust has a longstanding case law history that is proven in its effectiveness.

- Foreign trustees are not subject to U.S. court orders.

- Of the top 50 safest banks, only four are located in the U.S. There are much safer banks offshore than onshore.

What are the Legal and Financial Benefits?

As with trusts in general, that laws of each state determine the benefits which can come from establishing the DAPT or offshore asset protection trust (OAPT).

Those who set up the DAPT in a state with favorable laws can expect:

- Control over assets. Unlike traditional trusts of this kind which offer protection against creditors, the benefactor retains control over the assets as the discretionary beneficiary.

- Spendthrift clause. This not only blocks creditors’ access to assets. It also prevents the designated beneficiary from squandering the assets upon the benefactor’s death.

- Exclusion from the overall estate. For tax purposes, this trust is treated as a “stand-alone.”

- Serve as a type of prenuptial agreement. That can shield assets during a divorce. Unlike traditional prenuptial agreements, this one can be established unilaterally. That is, both parties do not have to approve it.

Scenarios for What the Asset Protection Trust Covers

Much of how DAPT is set up and the benefits it provides depends on particular state law. Those laws, though, can change. Currently the states considered most favorable to DAPT include Alaska, Delaware, Nevada, and South Dakota.

One scenario of how DAPT operates is the non-equity partner in a law firm. Her current net worth is about $2 million. In the legal sector, law-firm clients are increasingly suing the firm and individual attorneys for malpractice. Therefore, she takes the proactive step of “gifting” $500,000 of a non-qualified savings plan into the DAPT. She is the beneficiary. Those assets could grow in the spendthrift trust beyond the reach of those suing and be available to her when she retires. Also, creditors cannot touch the assets if she runs into other kinds of financial problems.

Another scenario is that she fears the firm, which is paying unusually high compensation to entry-level lawyers, could become insolvent in, say, five years. She intends to shield her assets from any bankruptcy judge order on behalf of the firm’s creditors.

A third scenario could pertain to the end of her marriage. The soon-to-be ex cannot go after the funds in DAPT as marital property.

A fourth is that the assets in trust could be growing, providing the income she needs when retiring.

Given the new tax law, she also benefits from the estate tax exemption that the law is increasing to $11 million from $5 million, adjusted for inflation, as of this writing. In 2029, the exemption, though, returns to $5 million, adjusted for inflation.

Factors to Consider Before Setting up a Spendthrift Trust

DAPT with spendthrift provisions is a sophisticated financial planning tool, with a complex legal framework.

There are many factors those focused on financial planning have to understand before choosing this strategy, as opposed to others.

Major Spendthrift Trust Considerations

New legal option. Because, unlike the offshore trust, the DAPT is relatively new there has not been a body of case law established. Therefore, if there are legal challenges to the provisions of the trust, the benefactor, that is, settlor, could lose. Those challenges might not only be in state law. One state, for example, may overrule the asset protection provisions of another state. “Great, so Nevada has those fancy trust laws. But you live here and are subject to your own state laws,” quips the California judge. Moreover, there could be a federal overlay. America is a litigious nation.

Yes, it is possible that creditors could gain access to the assets of a DAPT. It is much more difficult for your opponents to snatch the assets from your offshore trust.

The plaintiff in litigation could win the jury trial and be awarded $15 million. In a separate legal action that winner could have the court grant access to the funds in the trust to help pay that bill.

A divorcing spouse could contend and convince the court that the funds in the trust should be classified as marital property.

Limited availability.

Currently, DAPT is only legal in 17 states. Trust law mostly is the business of the state. The laws of those states regarding DAPT frequently vary significantly. Currently the states permitting it are:

Alaska

Delaware

Hawaii

Michigan

Mississippi

Missouri

Nevada

New Hampshire

Ohio

Oklahoma

Rhode Island

South Dakota

Tennessee

Utah

Virginia

West Virginia

Wyoming.

Can someone not residing in one of those states establish a DAPT? There is considerable legal uncertainty regarding that. The 2018 ruling in “Tangwall v. Wacker” increased those unknowns. The case was about a DAPT established in Alaska by residents of Montana, which does not permit that kind of trust. Their opponents alleged fraudulent transfer. Some interpret the ruling as indicating it is unwise to set up the DAPT in a state when not a resident. Many of us in the asset protection industry interpret the ruling as a warning to avoid DAPTs altogether and to exclusively utilize offshore asset protection trusts.

“Invasion” of assets.

The law varies from state to state. Some allow access to the funds for child support and for alimony. Others do not. Some specify that one can invade the trust only if the debts existed when the debtor transferred the funds into the trust. Therefore, this one should not use this as a legal strategy to avoid those kinds of obligations. Even in states favorable to DAPT where access in legally not permitted, there could be a court verdict in favor of the child or former spouse.

Offshore trusts, on the other hand are more flexible. Laws that define the Cook Islands trust or Nevis Trust specify that once the assets are in the trust for a specified period of time, the courts in these jurisdictions will not entertain challenges to the transfer of assets into the trust. So, once the court case in the U.S., for example is finished, the statute of limitations bars the suit in those jurisdictions.

Irrevocable.

This kind of trust is irrevocable. That is, it is one that the person who establishes it cannot alter it directly. They must go through the trustee to make changes, if any. Also, the person cannot retrieve from it all the assets. However, within that, in some states, there is “wiggle room.” For instance, in Nevada, the parties can make some modifications which are in the interests of the beneficiaries.

Suspicions about fraudulent transfer.

The protection of the assets only applies to legal actions launched after DAPT or offshore trust has been established. For pending claims by creditors some states and countries offer a one to two-year window for creditors to challenge the transfer of assets. This provision hinders fraudulent transfer behavior by the settlor. We must note that fraudulent transfer is a civil matter, not a criminal one. You cannot generally go to jail for it. It is simply moving assets so a creditor cannot touch them.

With an offshore trust, a fraudulent transfer accusation is a moot point. They are mere words on paper but cannot take your assets unless so ruled in the foreign court (in which there are skyscraper-sized barriers to proving so).

For example, distressed business owners anticipate filing for bankruptcy. Therefore, as an “end run” they will decide to set up a DAPT or offshore trust. That, they assume will put their assets out of the reach of the bankruptcy court. States are alert for such a maneuver.

However, all this is not black and white. There are states or countries, encouraging investment, which demand a high burden of proof from creditors contending fraudulent conveyance when the transfer of funds had been made into the DAPT or offshore trust. Those states want to be the ones in which the assets are maintained. So, their courts will favor the settlor.

Preventative, not curative.

As lawyers put it: DAPT is a preemptive tool. Those already immersed in financial problems will have a tough time protecting assets with this kind of spendthrift trust. An offshore trust is another story. Offshore trust law in the Cook Islands and Nevis do not recognize foreign judgments. We have established many an offshore trust for clients immersed in the heat of the battle.

Institutional trustee or board of directors.

Typically states require the appointment of either an institutional trustee such as a bank or trust company or a board of trustees. That means the benefactor, that is, the settlor, is not 100 percent in control.

But in some states the settlor does have these powers:

- Directing investment decisions

- Receiving income from the trust

- Receiving principal distributions in the trustee’s discretion

- Vetoing distributions to certain beneficiaries

- Replacing trustees

- Specifying the disposition of the trust assets when the settlor dies.

Conclusion

Building wealth does not necessarily bring with it in-depth understanding of how to ensure the next generation will not waste it. What is known as “ripping through a family fortune” is not uncommon. There is that old adage about shirtsleeves back to shirtsleeves within three generations.

Yes, estate planning is a complex field, both in terms of the law and in terms of financials. It is unreasonable to expect those transferring wealth to become experts. But what is necessary to learn can be accomplished by asking a lot of questions.

From those questions comes knowledge of options. The spendthrift trust is one of those options. It can be used along with other estate planning and financial planning tools to both preserve wealth and facilitate what benefactors want for their beneficiaries.

Want to set up a spendthrift trust or want to know more? You can utilize the numbers above or complete the consultation form located on this page for more information.