Do you want to prevent your assets from being used to pay for medical and nursing home care costs? Then, you must plan ahead. Should your resources permit you, purchasing long-term care insurance is one option. The problem is that it is the most expensive way to make sure ones assets will not end up financing a stay in a long-term care facility. As with any type of insurance, the earlier one has it in place the better. A typical policy as of this writing costs about $24,000 per year for a 55 year old single person and up to $72,000 per year for a 60 year old couple. They’ll typically need to start paying for it several years, even decades, before they actually need it. The earlier one get it the less expensive the monthly payments will be. A better option? A Medicaid Trust.

Key Points about Medicaid Trusts

- Your trust will own all of your other assets, including your home.

- You can still live in your home.

- US government Medicaid assistance will pay for your care, including nursing home costs, if required.

- Your assets need to be in the trust for five years before receiving Medicaid assistance (the 5-year lookback period).

- Your children can be the trustees of the trust.

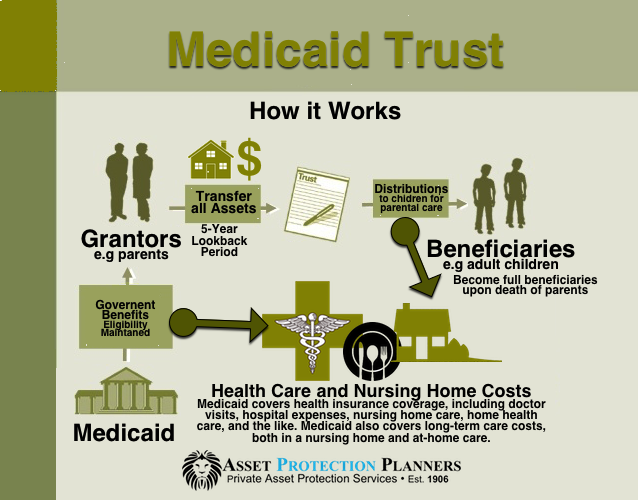

Medicaid Trust

Creating a Medicaid Trust, is a much less expensive option. A Medicaid Trust, sometimes erroneously called a Medicare Trust, is an irrevocable trust. It holds the assets of the future nursing home patient. You must have a properly worded trust. Your Medicaid Trust must have an a trustee, which can be your children, other relative, or an independent third party. The Administration on Aging or AOA , a division of the U.S. Department of Health and Human Services, says, “This is the only kind of trust that is exempt from rules regarding trusts and Medicaid eligibility.” To make sure Medicaid will not disallow any assets you include in the trust, you must set it up and transfer assets into it at least five years prior to entering a nursing home or applying for long-term care. We call this the five-year look back period.

Some people make the big mistake of giving assets away to family members instead of creating a trust. One big problem with this scenario is that it can create a tremendous gift tax bill. If the same family member received the assets after the parent or grandparent died, there would likely be no tax bill. That is, unless the assets were in the multi-millions. Other, perhaps larger problems arise when the child or grandchild who has received the house, car and bank account. Say someone sues them. Perhaps they run into a tax problem, die, divorce or incur a huge hospital bill. Grandma’s home, automobile and accounts could be confiscated. Those are some additional reasons why a much better option is the Medicaid trust. Moreover, this type of trust is a valuable part of of estate planning. It can help you avoid the expensive and time-consuming probate process.

How Medicaid Trusts Work

You place your assets into an irrevocable Medicaid trust. The future Medicaid recipient can use the assets as before. However, the trust holds the assets instead of the recipient. Therefore, the government does not count those assets for qualification purposes. So, grandma can still live in the house, use the furniture and drive the car held by the trust. Nevertheless, grandma will not hear “your assets are too valuable to qualify for the program.” This is because the assets will not be in grandma’s name. In addition, there generally are provisions in the trust so that her kids and grandkids, etc. can receive the assets after her passing.

The Perils of Long-term Care Insurance

As people live longer, paying for long-term care insurance becomes more expensive. In the United States, less than 8 percent have long-term care insurance. The prohibitive cost and varying coverage restrictions are often enough to deter the average American. So, most do not purchase long-term care insurance. Additionally, many people are in denial about needing long-term care when they get older. That’s something that happens to ‘other people.’ The truth, however, is quite grim. According to data released by the Center for Retirement Research, the odds that older Americans will need some type of long-term care or assistance are up to 58 percent for women and 44 percent for men.

The cost for a nursing home stay or home health care vary greatly from one state to the next. But older Americans can expect to pay tens of thousands of dollars each year for long-term care; no matter where in the country they live. This can come out of their own pockets, Medicaid, or paid for by a long-term insurance policy. The cost is expected to keep getting higher with each passing year. In light of this scenario, purchasing long-term care insurance several years before you reasonably expect to need adds up to a very expensive option. One is almost always better off financially to set up a Medicaid Trust and invest the money that would have gone toward the premiums.

Protect Assets from Nursing Home Costs

There are ways to mitigate the cost of long-term care insurance and protect more of your assets from nursing home costs. For example, you could buy a plan with a limited coverage. Then pay for what the plan does not cover from your savings. Or, you can opt for a reduced daily benefit or even limit the number of years benefits are paid. If you can afford to do so well in advance of needing long-term care (ideally, when you’re young and in good health), purchasing long-term care insurance might be sensible and prudent. However, it is a very expensive way to ensure that your assets will not be used to pay for long-term care, should you end up needing it when you’re older.

Moreover, there is always the possibility that you may not ever get to collect on a long-term care insurance policy. This is because you may end up not needing long-term care (good for you!). The industry does offer options, such as life insurance policies that come with long-term care benefits. If you pass away without using the long-term care benefits, your heirs receive the death benefit. This is just as they would with a typical life insurance policy. However, if you need to avail of the long-term care benefits, you can use the death benefits. This may pay for whatever long-term care you need. If there is anything left after you pass away, that goes to your heirs as well.

Long-Term Care from Medicaid

Majority of Americans will end up relying on Medicaid for their long-term care. However, before you qualify for long-term care from Medicaid, your existing financial resources must meet the set threshold. The problem is that this threshold level is extremely low. Some states require Medicaid recipients to have no more than $2,000 in savings and less than $50 a month in income in order to qualify. What happens to Americans who need long-term care who cannot afford long-term insurance? Plus, what if they do have certain assets that puts them above the Medicaid threshold?

It often happens that elderly Americans ‘spend down’ their financial resources. They do this so they can meet the Medicaid threshold and qualify for long-term care. This means they pay for long-term care out of their own resources. Once depleted, there may be such a time when they can qualify for Medicaid. The problem is that spending down your assets and financial resources to qualify for Medicaid long-term care means there’s nothing you can leave behind. When you die, your children and spouse may be left with nothing, with the possible exception of your house. But this is only for as long as the value of your property meets the maximum allowable value. This is established by the state where you live. If your house is assessed to be above this maximum allowable value, you could still lose it in some states.

Medicaid Five Year Lookback Period

Additionally, Medicaid has a five-year look-back window. This timeframe is for assets that you transfer to a trust or “sell.” People who do this typically sell them for below market value. And then sell them family members and/or friends before applying for long-term care. Transfers of certain assets may be disallowed if they are made less than five years before you enter a nursing care or assisted living facility. If they are disallowed, that means you still own them. Therefore, you have to spend them down before you can qualify for Medicaid long-term assistance.

Irrevocable Medicaid Trust

Understandably, you may have certain assets that you wish to leave behind for your children or spouse when you die. One way to avoid spending down your assets so you can qualify for Medicaid: Create an irrevocable Medicaid trust. The assets you use to fund this trust will not be counted for Medicaid eligibility. This is as long as neither you (the person applying for Medicaid) nor your spouse has direct access to the principal or is named as the trustee.

Set up properly, an irrevocable Medicaid trust protects your assets from a Medicaid spend down. It allows you to qualify for long-term care at the same time. It also means your assets can pass down to your spouse and children when you die. That is, if it is so stated in the terms of the trust. Keep in mind however, that you have to establish this trust early. Then transfer assets to it at least five years before you apply for Medicaid long-term care benefits. If you do not meet this five-year minimum, Medicaid may judge your transfer and the trust itself as void, and so will count your assets in determining your eligibility (or ineligibility) for long-term care.

The Goal

The goal of a Medicaid Trust is to dissociate you from your assets. That way, they will not be considered in determining your eligibility for long-term care from Medicaid. In this respect, almost any type of domestic or offshore irrevocable trust will basically accomplish the same goal as a Medicaid Trust. However, keep in mind that these asset protection vehicles may fall under a completely separate set of rules and regulations. It’s best to do your homework. Get advice and consult with a trusted professional. And do both at the earliest possible time you can.

According to the U.S. Department of Health and Human Services, more than 70 percent of Americans over the age of 65 will need some type of long term care assistance at some point in their lives. Forty percent of Americans who reach 65 will likely enter a nursing home facility. And this is just is one type of long-term care (there are others). For 20 percent of these elderly Americans, the average stay in a nursing home typically lasts for five years. While most Americans think long-term care is something that others will need (and not them), these grim statistics clearly say otherwise.

Play by the Rules

Nobody is ever advised to purposely attempt to defraud Medicaid by hiding assets from nursing home costs through illegal means. However, protecting your assets from Medicaid through trusts is a perfectly legal and, in fact, a financially shrewd maneuver.

Purchasing long-term care insurance several years before you may realistically expect to benefit from it is an extremely expensive way to protect your assets from a Medicaid spend down. Long-term care insurance is often extremely costly. The industry also offers wealth-sapping hybrid options that combine a life insurance policy with long-term care benefits. If you end up needing long-term care, you can draw down the death benefits. Then use them to pay for nursing home costs or extended home care assistance. If you don’t end up needing long-term care, your heirs receive death benefits when you die. This is just as it is with a regular life insurance policy.

Less Expensive Option

Setting up a Medicaid Trust is a much less expensive option. Keep in mind, to make sure Medicaid will not disallow any assets included in the trust, set it up early. That is, at least five years prior to entering a nursing home or applying for long-term care.

Conclusion

No one wants to think of ever needing long-term care. But the truth is, this happens much more often and to far more people than we realize or care to admit. Take the steps to make sure your assets are legally safeguarded from nursing care costs. Doing so means you have a higher chance of being eligible for Medicaid long-term care benefits. It also means, you get to leave something behind for the people you care about the most.

Related Articles