What is asset protection? Merriam-Webster provides two interesting definitions for the word asset: “an item of value owned” and “something useful in an effort to foil or defeat an enemy.” It defines protection, in this context, as “to save from contingent financial loss.” Putting the definitions together, we have something to the effect of the act of saving an item of value from financial loss.” As such, your legal enemies, creditors and claimants, could come after your valuable property, including your bank accounts, at any time. So, how can you protect yourself? To the point, an asset protection trust is one of the strongest legal tools to shield assets from creditors.

Establishing a trust for your high-value assets is an important part of a full asset protection plan. There are a lot of different kinds of trusts to choose from, but not all of them are effective in shielding your assets from creditors. In this article, we’ll explore what an asset protection trust is, a few different types of these trusts, and how you can establish one for your assets.

Defining the Terms

How does an asset protection trust work? To find out, let’s take apart those two key phrases, “asset protection” and “trust.” As an additional definition to the one we gave above, Investopedia defines asset protection as a concept of and strategies for guarding one’s wealth. It is a part of financial planning that is specifically intended to protect assets from creditor claims, judgments, and other losses. Both individuals and business entities use an asset protection plans. As such, they limit creditor access to some of their valuable assets while still operating within debtor-creditor law. The most effective asset protection plans are put in place before a claim or liability occurs. It is not too late to create protections after a claim is in progress. It is, however, more effective. That is, the earlier the better.

There are many types of trust. Here, we are focusing on the type that provides asset protection. In a trust, one party, known as a trustor or grantor, gives another party, the trustee, the right to hold the title to property or assets. The trustee fulfills this responsibility for the benefit of a third party, the beneficiary. This type of relationship, in which one person or organization acts on the behalf of another to manage assets, is a fiduciary relationship. Trusts provide legal protection for a trustor’s assets. A trust can also ensure the distribution of those assets as per the wishes of the trustor, reduce paperwork, save time, and sometimes avoid or reduce inheritance or estate taxes.

Revocable and Irrevocable Trusts

As stated, there are many different kinds of trusts, but all of them fall into two categories: revocable or irrevocable. Only one of them is good for asset protection trust planning, however. As The Balance explains, a revocable trust is a type of trust that the settlor can change at any time. Trust amendments allow for the trustor to make changes to provisions, beneficiaries, and more after he or she establishes the trust. The settlor can also revoked the trust at any time.

As appealing as this sounds, revocable trusts are not generally good for asset protection. The law considers assets in a revocable trust as your personal assets. Creditors and estate taxes continue to include those assets. Thus, revocable trusts have virtually no creditor protection when lawsuits strike. A benefit to this type of trust is the avoidance of probate for the assets they hold. Assets pass directly to beneficiaries, avoiding courtroom procedures. This trust can also be a good idea in planning for a future mental disability. That is, it can appoint someone else to take over the assets when the trustor is no longer able to.

Conversely, a trustor cannot directly change an irrevocable trust he or she establishes it. Once parties sign the agreement, the trust formed and funded. Afterwards, settlor cannot effect changes single-handedly. With some trusts, the settlor can make changes requests to the trustee. Assets placed in an irrevocable trust can enjoy protection from creditors and are no longer considered part of your personal or business assets. As the best form of asset protection, the rest of this article will focus on different types of irrevocable asset protection trusts.

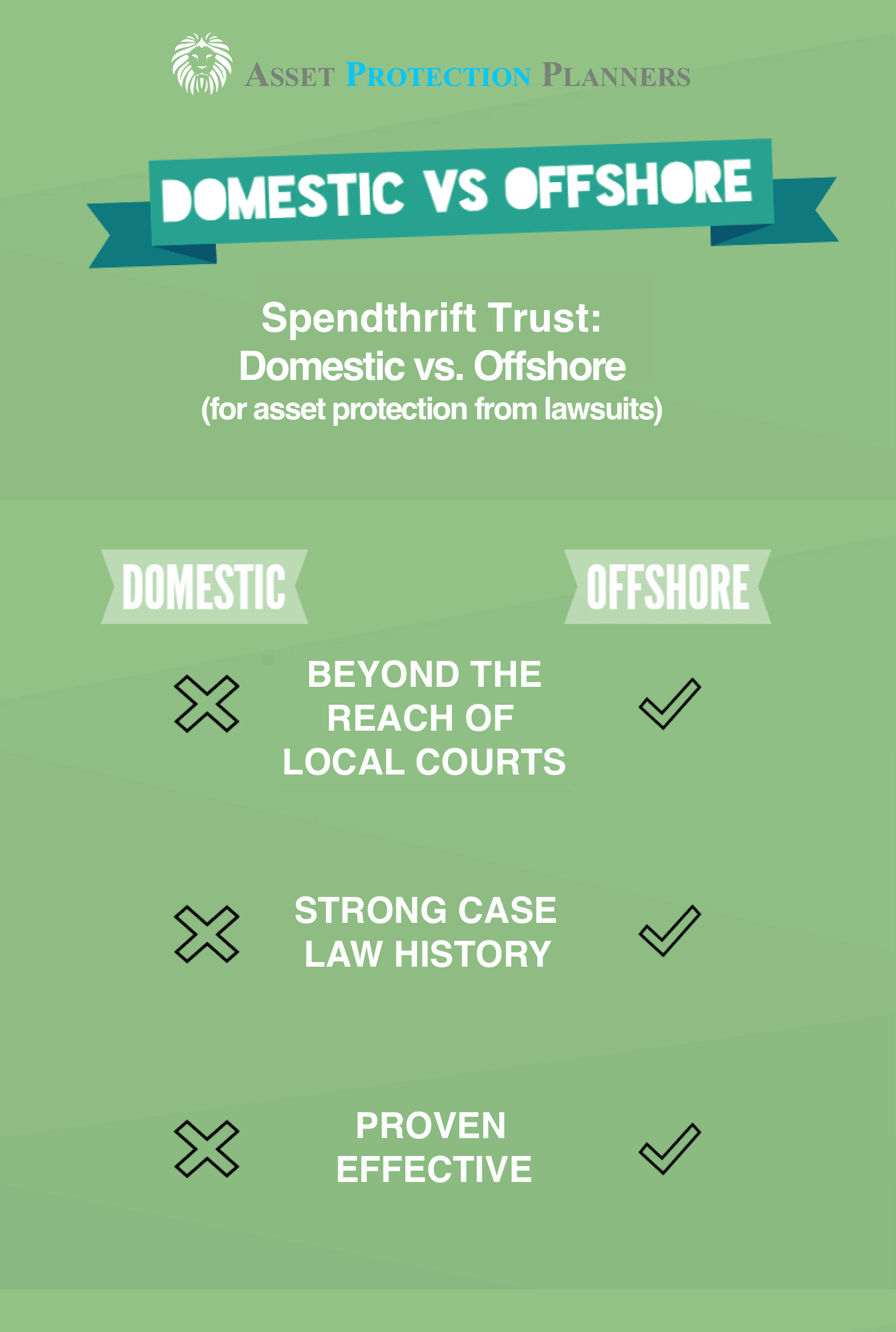

Domestic and Foreign Asset Protection Trusts

When creating a standard asset protection trust, you can create it domestically or in a foreign country. Which option is better? The answer is that it depends on how much protection you need, and which benefits are most appealing.

A domestic asset protection trust, as the name suggests, is a tool used to shield personal assets within the United States, according to Jiah Kim & Associates. What states allow asset protection trusts? Not all of them, but Alaska, Delaware, and Nevada were among the first to offer domestic asset protection trusts. They remain the most popular choices today.

Domestic Trust

A domestic asset protection trust cost is more affordable than a foreign trust, and it is widely recognized by state and federal courts across the country. Knowing where your trust is allows you to easily follow any legal or economic developments that may impact your trust. These trusts are not immediately effective, however, and creditors have been challenging them more recently. There can be confusion if the trust is set up in a different state than you or the asset. Moreover, creditors have made cases of some transfers into these trusts as being fraudulent. Frankly, case law doesn’t look very good regarding domestic asset protection trusts.

Offshore Trusts

Foreign or offshore asset protection trusts are, at their heart, meant for the same thing as a domestic asset protection trust. Creating a trust overseas, however, comes with significantly more powerful asset protection benefits. Some foreign countries don’t acknowledge US judgments. This includes the Nevis trust, Cook Islands trust and Belize trust. The laws of the country in which one established this valuable legal tool governs the trusts. U.S. laws and court rulings do not dictate the actions of the offshore trustees. A U.S. court says “give me the money.” Unlike his domestic counterpart, the offshore trustee can say, “sorry, not going to.” There is a great deal of privacy that comes with a foreign trust as well. U.S. subpoenas for trustee records fall on deaf ears. “Sorry, you don’t have jurisdiction down here,” in effect, says the your foreign trustee.

These assets are more protected from seizure in an offshore trust than a domestic trust; far more protected. Plus, when we put an offshore LLC inside of the trust, the LLC acts as your remote control to the trust assets. So you hold your bank account in the LLC name. The trust owns the LLC. You are the account signer before legal duress. Your trustee takes this role when you are under legal attack. Thus, it is an easy and fast transition when needed.

The strongest offshore trusts are in Nevis. Then Cook Islands and Belize come in second and third.

Family Protection Trusts

When it comes to estate planning, a family protection trust can be vital. Margolis & Bloom, LLP describes this irrevocable trust often is set up by parents with their children as beneficiaries. A family protection trust holds the inheritance instead of distributing all the assets outright when the parent(s) pass.

There are a lot of benefits to a family protection trust for the beneficiaries. The trust can protect these funds from bankruptcy, divorce, and other creditor claims. Since the child’s estate doesn’t include these funds, they avoid double taxation. This asset protection tool provides a lot more protection than trusts one creates in the children’s own names. If the intended beneficiary of the trust passes, funds stay in the family for the beneficiary’s children. This trust also allows for specific management of the assets for recipients who might need assistance in managing the funds.

Family asset protection trust disadvantages can include high fees. Once funded, these trusts must file their own tax return every year, although they do not pay taxes. If the child or beneficiary is also the trustee, they can eliminate the trust’s protections. This can be a vulnerable situation, which is why it is best, from an asset protection standpoint, to appoint an independent trustee.

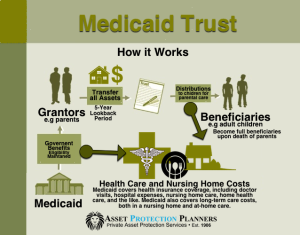

Medicaid Asset Protection Trusts

If applying for Medicaid might be in your future, a Medicaid Asset Protection Trust (MAPT) is a good tool to have. As The American Council on Aging explains, MAPTs are a valuable for people looking to maintain or acquire eligibility status for Medicaid. Applicants for Medicaid are limited on the amount of assets they can possess, and an MAPT protects those excess assets. It allows someone who would otherwise be ineligible for Medicaid the opportunity to receive the care they need at home or in a nursing home. MAPTs can also protect assets for children and other relatives.

Although there is some variance by state, the asset limit for a Medicaid applicant requesting long-term care is currently $2,000. Some higher value assets receive exemptions to this like one’s primary residence, a vehicle, and wedding rings. However, that still leaves many applicants with assets that are too high. Many applicants with an excess of assets still can’t afford their care. The excess needs to be “spent down” or put into a Medicaid qualifying trust like an MAPT.

Medicaid Trust Must be Irrevocable

In order to be exempt for Medicaid eligibility requirements, the MAPT must be irrevocable. The principal beneficiary must be someone other than the trustor. Trustees cannot be either the trustor or their spouse, but adult children and other relatives can be. Medicaid looks back at the last five years of an applicant, so an MAPT must be set up before that in order to be effective.

If you’re trying to find out how to protect assets from Medicaid recovery, an MAPT is your best choice for that as well. When a Medicaid recipient passes away, the state in which they resided attempts to collect reimbursement for what it paid for long-term care. The state cannot come after those assets that are already in an MAPT. The trustor can no longer directly access a trust like this and the original owner does not own the anymore. The trust does. That is because if they did, they would not be eligible for Medicare. That is not to say they cannot use them. It is that they do not directly own them.

You can still live in your house, for example, though the trust owns the house. The trust can buy your food and pay your bills for you, for example. So, you have access to the benefits of the trust through your trustee but, for eligibility purposes, you don’t own them firsthand.

Setting Up Your Trust

The enemies to your assets are many: creditors, claims, bankruptcy, divorce, and so much more. When you’re ready to keep those assets safe – and maybe earn a few other benefits along the way – talk to one of our experienced consultants. We can help explain your options in more depth and walk you through setting up your trust. There is no easy asset protection trust template, and the process to set up an effective asset protection trust can be complicated. Get the experts on your side and use the contact information on this page to talk to